Who is mandatorily subject to tax audit?

| Category of person | Threshold |

|---|---|

| Carrying on business which is declaring profits as per presumptive taxation scheme under Section 44AD | If the total sales, turnover or gross receipts does not exceed Rs 2 crore in the financial year, then tax audit will not apply to such businesses. |

Who is eligible for Section 44AB?

Applicability under section 44AB Any person pursuing business and whose total turnover or gross receipts exceed a sum of 2 Crore rupees in any previous year (However, this provision is not applicable to the persons who opts for presumptive taxation scheme).

What is the ITR 3?

The ITR 3 is applicable for individual and HUF who have income from profits and gains from business or profession. The persons having income from following sources are eligible to file ITR 3 : The return may include income from House property, Salary/Pension, capital gains and Income from other sources.

Are you audited u/s 44AB * Yes No?

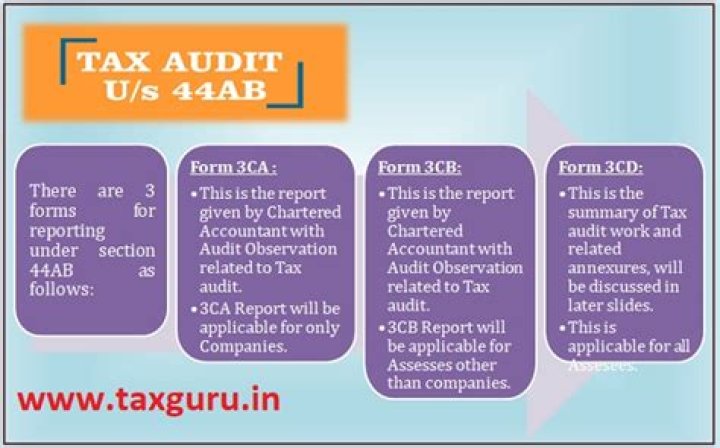

Specified books of account as per Rule 6F

| Taxpayer | Profit/Loss | Whether books as per section 44AA applicable |

|---|---|---|

| BusinessSales, turnover, gross receipts | Profit/Loss | No |

| BusinessTurnover | Profit | No |

| BusinessTurnover | Loss | No |

| BusinessTurnover | Profit/Loss | Yes |

What is 115BAC in income tax?

The Budget 2020 introduced a new regime under section 115BAC giving an option to individuals and HUFs to pay income tax at lower rates. From FY 2020-21, the assessee can choose to pay income tax under an optional new tax regime.

Are you audited u/s 44AB means for salaried?

Section 44AB gives the provisions relating to the class of taxpayers who are required to get their accounts audited from a chartered accountant. The audit under section 44AB aims to ascertain the compliance of various provisions of the Income-tax Law and the fulfillment of other requirements of the Income-tax Law.

Who is not eligible for 44AD?

The presumptive taxation scheme of section 44AD can be opted by the eligible persons, if the total turnover or gross receipts from the business do not exceed Rs. 2,00,00,000. In other words, if the total turnover or gross receipt of the business exceeds Rs. 2,00,00,000 then the scheme of section 44AD cannot be adopted.

Are you audited under 44AB?

Ans. As per section 44AB, following persons are compulsorily required to get their accounts audited : A person carrying on business, if his total sales, turnover or gross receipts (as the case may be) in business for the year exceed or exceeds Rs. 1 crore.

What is 44AB in income tax?

Section 44AB of the Income Tax Act is applicable for individuals who meet certain requirements and have to get their accounts audited by a Chartered Accountant. This practice is done solely to help the Assessing Officer with the calculation and computation of the total taxable income of the individual in question.

What is Section 44AB?

Amendment w.e.f., 01st April 2019 – To reduce the compliance burden on small and medium enterprises, section 44AB is proposed to amended to increase the threshold limit, for a person carrying on business, from Rs. 1 crore to Rs. 5 crores.

What is Section 44AB(E) of Income Tax Act for Ay 2022-23?

Section 44AB gives the provision relating to the class of taxpayers who are required to get their account audited from a chartered accountant. In this article, we will try to clear all doubts regarding the applicability of Section 44ab (e) of the Income Tax Act For AY 2022-23.

What is the turnover limit under Sec 44AB and SEC 44AD?

Under Budget 2021, the turnover limit under Sec 44AB has been increased from INR 5 Cr to INR 10 Cr. However, the turnover limit under Sec 44AD has not been changed. When the Trading Turnover is between INR 2 Cr and INR 10 Cr, neither Sec 44AB is applicable nor Sec 44AD. Thus, Tax Audit is not applicable irrespective of profit or loss.

When is a business loss subject to tax audit under Section 44AB?

In case of loss from business when sales, turnover or gross receipts exceed 1 crore, the taxpayer is subject to tax audit under 44AB. Carrying on business (opting presumptive taxation scheme under section 44AD) and having a business loss but with income below basic threshold limit. Tax audit not applicable.