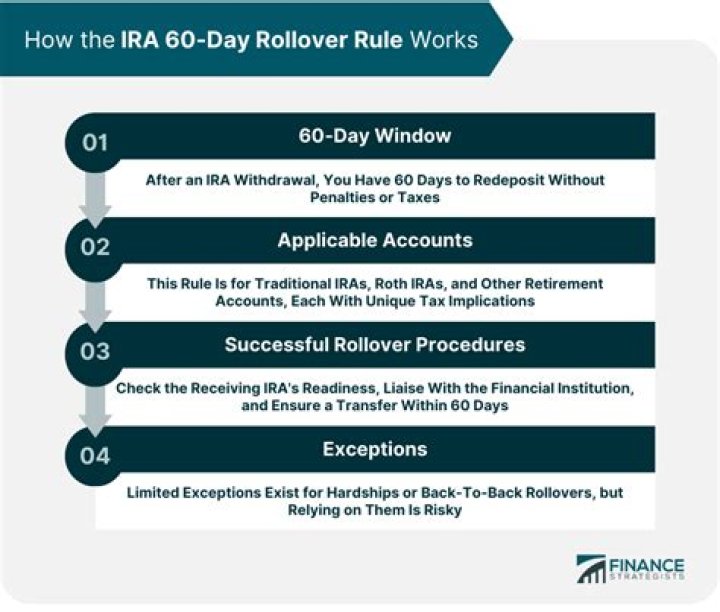

A “60-day rollover” occurs when you receive a distribution from your IRA, and deposit the money into another IRA or back into the same IRA within 60 days. If you comply with the 60-day deadline, the distribution is not taxed. If you miss the deadline, you will owe income tax, and perhaps penalties, on the distribution.

How do you count days for a 60 day rollover?

But how do you know when the 60 days are up? You do NOT start counting from the date you request the distribution, the date on the check, or the date the funds left the IRA account. You start counting on the date you receive the funds if they are mailed, or the date they hit your bank account if they are transferred.

Can you put money back into an IRA after 60 days?

You can put funds back into a Roth IRA after you have withdrawn them, but only if you follow very specific rules. These rules include returning the funds within 60 days, which would be considered a rollover. Rollovers are only permitted once per year.

How do I report a 60 day rollover on my taxes?

To report a 60 day rollover on your taxes, your plan’s administrator will send you a 1099-R. In box 13 of the 1099-R is the date of payment or when the funds were withdrawn from the 401(k). That is the date the IRS uses to determine whether the funds were deposited within 60 days.

Is a 60 day rollover taxable?

No taxes will be withheld from your transfer amount. 60-day rollover – If a distribution from an IRA or a retirement plan is paid directly to you, you can deposit all or a portion of it in an IRA or a retirement plan within 60 days.

Does the 60 day rollover rule apply to direct rollovers?

Under recently revised IRS rules, you can make only one tax-free, 60-day, rollover from any IRA you own (traditional or Roth) to any other IRA you own in any 12-month period. However, this limit does not apply to direct rollovers or trustee-to-trustee transfers.

Do IRA rollovers need to be reported to IRS?

An eligible rollover of funds from one IRA to another is a non-taxable transaction. Even though you aren’t required to pay tax on this type of activity, you still must report it to the Internal Revenue Service. Reporting your rollover is relatively quick and easy – all you need is your 1099-R and 1040 forms.

How do I report an IRA rollover on my taxes?

Your rollover is reported as a distribution, even when it is rolled over into another eligible retirement account. Report your gross distribution on line 15a of IRS Form 1040. This amount is shown in Box 1 of the 1099-R. Report any taxable portion of your gross distribution.

How do I file a 60 day rollover on my taxes?

Are IRA rollovers reported on tax return?

What is the 60 day rule for IRA?

The 60-day rollover rule simply means that an employee have 60 calendar days from the date the check is received in order to deposit the funds to his new retirement account, or IRA, for instance. It is very important, moreover, to be familiar with the requirements of the receiving financial institution, such as documentation from the prior plan.

What to do with a rollover IRA?

A rollover takes three steps: Open the appropriate IRA.*. Move your money to Fidelity—to do this, you will need to initiate a rollover from your former employer’s plan. Choose your investments in the Rollover IRA. Call 800-343-3548 and a rollover specialist will help you every step of the way.

What is the 60 day rule?

The 60 day rule is one of the only ways an owner has access to money in a retirement account without paying taxes or penalties on the distribution.

Can an IRA distribution be put back?

The IRS allows you a 60-day window to put back any distributions taken from an IRA. When you take a distribution from your IRA, you do not have to specify whether you are taking a permanent distribution or whether you are merely rolling the money over.