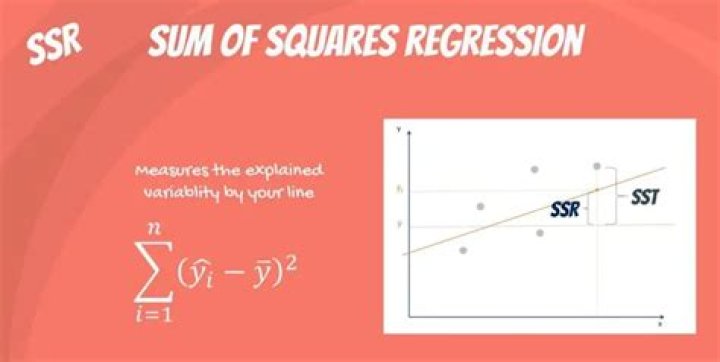

Sum of Squares Regression (SSR) – The sum of squared differences between predicted data points (ŷi) and the mean of the response variable(y).

What is SSE and SSR in regression?

SSR is the additional amount of explained variability in Y due to the regression model compared to the baseline model. The difference between SST and SSR is remaining unexplained variability of Y after adopting the regression model, which is called as sum of squares of errors (SSE).

Is SSR and r2 the same?

R Squared is the ratio between the residual sum of squares and the total sum of squares. SSR (Sum of Squares of Residuals) is the sum of the squares of the difference between the actual observed value (y) and the predicted value (y^).

How do you calculate SST and SSR?

SST = SSR + SSE….We can also manually calculate the R-squared of the regression model:

- R-squared = SSR / SST.

- R-squared = 917.4751 / 1248.55.

- R-squared = 0.7348.

How do you calculate SSR and SST?

SSR = Σ( – y)2 = SST – SSE. Regression sum of squares is interpreted as the amount of total variation that is explained by the model. r2 = 1 – SSE/SST = (SST – SSE)/SST = SSR/SST the ratio of explained variation to total variation.

What is SSE regression?

What is the SSE? The last term is the sum of squares error, or SSE. The error is the difference between the observed value and the predicted value. We usually want to minimize the error. The smaller the error, the better the estimation power of the regression.

What is SST SSR?

1. Sum of Squares Total (SST) – The sum of squared differences between individual data points (yi) and the mean of the response variable (y). 2. Sum of Squares Regression (SSR) – The sum of squared differences between predicted data points (ŷi) and the mean of the response variable(y).

What does SSR measure?

What is the SSR? The second term is the sum of squares due to regression, or SSR. It is the sum of the differences between the predicted value and the mean of the dependent variable. Think of it as a measure that describes how well our line fits the data.

How do you calculate SST and SSR in R?

How to Calculate SST, SSR, and SSE in R. We often use three different sum of squares values to measure how well a regression line actually fits a dataset: 1. Sum of Squares Total (SST) – The sum of squared differences between individual data points (yi) and the mean of the response variable (y). SST = Σ (yi – y)2. 2.

What is SSR and SSE in statistics?

Sum of Squares Regression (SSR) – The sum of squared differences between predicted data points (ŷi) and the mean of the response variable (y). SSR = Σ (ŷi – y)2 3. Sum of Squares Error (SSE) – The sum of squared differences between predicted data points (ŷi) and observed data points (yi).

What is the sum of squared differences in SSR?

Sum of Squares Regression (SSR) – The sum of squared differences between predicted data points (ŷ i) and the mean of the response variable(y). SSR = Σ(ŷ i – y ) 2 3.

How do you calculate SSR esidual?

From these Wikipedia definitions: So if the model explained all the variation, SSR esidual = ∑ ( y i − y ^ i) 2 = 0, and R 2 = 1. Suppose r = 0.7 then R 2 = 0.49 and it implies that 49 % of the variability between the two variables have been accounted for and the remaining 51 % of the variability is still unaccounted for.