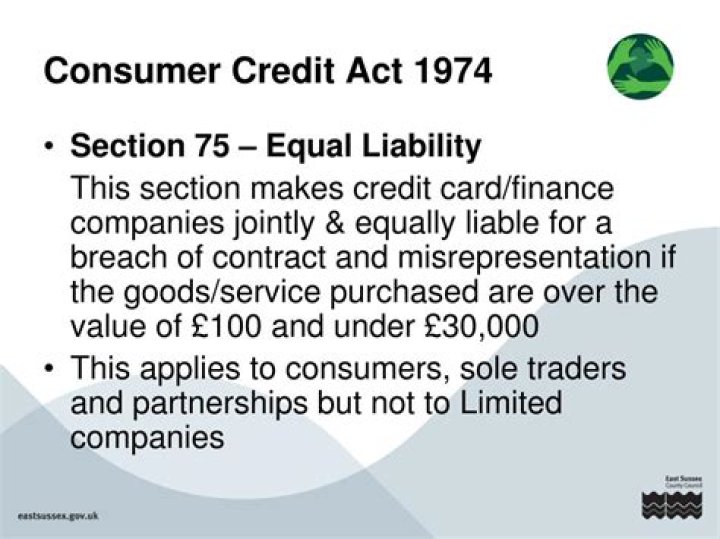

What is Section 75? It’s part of the Consumer Credit Act 1974 that means your credit card provider is jointly and severally responsible for any breach of contract or misrepresentation by a retailer or trader.

Is there a time limit on section 75 of the Consumer Credit Act?

While there is no time limit for making a claim under Section 75, the statute of limitations in the UK is six years (and is five in Scotland). Meaning if you were to pursue a Section 75 refund through the courts, this is the amount of time you would have to do so.

How do I claim Section 75 of the Consumer Credit Act?

How do I make a claim?

- Contact the retailer: It’s usually far easier to get a refund from the retailer, so this should be your first option.

- Call your credit card provider: Tell them you want to make a claim under Section 75 of the Consumer Credit Act.

- Fill out a claim form:

How does a section 75 claim work?

What does Section 75 cover? Section 75 is fantastic protection – if you order something and the retailer goes kaput, you can still claim your money back from the credit card provider (even if you’ve since closed your credit card account). Section 75 applies to most, but not all, credit card agreements.

What can I claim for under section 75?

Under Section 75 of the Consumer Credit Act, your credit card company is jointly liable if something goes wrong with a product or a service you’ve paid for by credit card. You can potentially claim for any breach of contract or misrepresentation by the company from which you’ve bought your goods.

How long does a company have to respond to a section 75?

The provider will then have eight weeks to respond to this complaint. If the provider does not respond or refuses to pay out, you can refer your claim to the Financial Ombudsman Service (FOS).

Does the Consumer Credit Act apply to debit cards?

Debit card payments and purchases are not covered by section 75 of the Consumer Credit Act. This might cover purchases of any value made on debit, credit or prepaid cards.

How long does Section 75 cover you for?

There’s no legal time limit for your card provider to resolve a section 75 claim although it’s reasonable to expect a maximum of 28 days. But keep in mind its legal responsibilities during this time go beyond just making its own attempt to recover your loss from the retailer – it is equally liable for the entire sum.

Can you claim Section 75 on a debit card?

Can you do section 75 on a debit card?

Can I make a section 75 claim online?

The quickest way make a Section 75 claim is to claim online.

Does section 75 CCA 1974 apply to credit card purchases?

As no credit is used, Section 75 CCA 1974 does not apply to that purchase. However, there is a mechanism available to you, for your card issuer to reclaim money from the retailer’s bank. This is known as the Chargeback procedure.

What is section 75 of the Consumer Credit Act?

Section 75 of the Consumer Credit Act is meant to provide vital cover if something goes wrong with a purchase, but a loophole could leave you out of pocket. Now, the Financial Ombudsman Service has called for reform.

How can section 75 claims help you?

In Summary, How Can Section 75 Claims Help You? Section 75 of the Consumer Credit Act 1974 says that a credit card company is ‘jointly and severally liable’ for any breach of contract or misrepresentation by the company to which you have paid money for goods and services.

Does section 75 cover credit card withdrawals?

If you use your credit card to withdraw cash for a particular purchase, you won’t be covered by Section 75 as there’s no link between the credit card company and the retailer. Cash withdrawals usually attract a fee and a much higher interest rate anyway, so they’re best avoided on the whole.