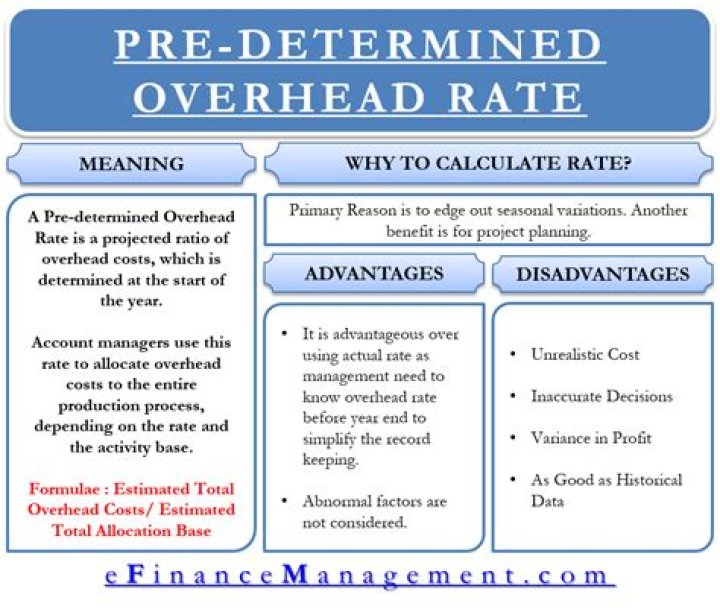

A predetermined overhead rate is an allocation rate that is used to apply the estimated cost of manufacturing overhead to cost objects for a specific reporting period. However, the use of multiple predetermined overhead rates also increases the amount of required accounting labor.

What is predetermined overhead rate and example?

Predetermined Overhead Rate = Estimated Overhead Cost/Estimated Units to be Allocated. Source: Predetermined Overhead Rate (wallstreetmojo.com) The Overhead costs. Examples include rent payable, utilities payable, insurance payable, salaries payable to office staff, office supplies, etc.

What is factory overhead in business?

Factory overhead is the costs incurred during the manufacturing process, not including the costs of direct labor and direct materials. Factory overhead is normally aggregated into cost pools and allocated to units produced during the period.

Why is predetermined overhead rate important?

Predetermined rates make it possible for companies to estimate job costs sooner. Using a predetermined rate, companies can assign overhead costs to production when they assign direct materials and direct labor costs.

What are the major reasons for using predetermined overhead rates?

The primary advantage of a predetermined overhead rate is to smooth out seasonal variations in overhead costs. These variations are to a large extent caused by heating and cooling costs, which, while high in the summer and winter months, are relatively low in the spring and fall.

How is a predetermined factory overhead rate calculated?

A predetermined overhead rate is calculated at the start of the accounting period by dividing the estimated manufacturing overhead by the estimated activity base. The predetermined overhead rate is then applied to production to facilitate determining a standard cost for a product.

Why do companies use predetermined overhead rate?

What is the predetermined overhead rate formula?

The predetermined overhead rate is set at the beginning of the year and is calculated as the estimated (budgeted) overhead costs for the year divided by the estimated (budgeted) level of activity for the year. This activity base is often direct labor hours, direct labor costs, or machine hours.

Which is not factory overhead?

Salary is not factory overhead.

How do you use predetermined overhead rate?

With the manufacturing overhead costs and the machine hour totals, you can calculate the predetermined overhead rate by dividing the overhead costs by the machine hours. For instance, if the manufacturer estimates $10,000 in overhead costs with 20,000 machine hours, the predetermined overhead rate is 50 cents per unit.

What is a predetermined overhead rate in manufacturing?

When companies begin the planning process of manufacturing a product, cost projections are a large and important focus. Calculating a predetermined overhead rate is one of the first tasks management will take on because it provides a formula to estimate the production costs of a product in advance.

How do you calculate predetermined overhead rate formula?

The predetermined overhead rate formula is calculated by dividing the total estimated overhead costs for the period by the estimated activity base. Take direct labor for example.

What is the predetermined manufacturing overhead cost of the GX company?

The budget of the GX company shows an estimated manufacturing overhead cost of $8,000 for the forthcoming year. The company estimates that 1,000 direct labors hours will be worked in the forthcoming year. Using the above information, we can compute the predetermined overhead rate as follows:

How do you calculate manufacturing overhead cost?

If $420,000 is estimated manufacturing overhead cost for a period and the company uses machine hours as the activity driver (see first paragraph of the main article), then you need to divide $420,000 by 60,000 hours. The predetermined overhead rate would be $7.00 per machine hour as calculated below: = $420,000/60,000 = $7 per machine hour