Value at risk (VaR) is a commonly used risk measure in the finance industry. Monte Carlo simulation is one of the methods that can be used to determine VaR. There are two things we need to specify when stating value at risk: The time horizon. The time horizon is accounted for in the portfolio model.

What is Monte Carlo simulation VaR?

3. Monte Carlo Simulation. The third method involves developing a model for future stock price returns and running multiple hypothetical trials through the model. A Monte Carlo simulation refers to any method that randomly generates trials, but by itself does not tell us anything about the underlying methodology.

What is Monte Carlo simulation in risk management?

Monte Carlo simulation performs risk analysis by building models of possible results by substituting a range of values—a probability distribution—for any factor that has inherent uncertainty. It then calculates results over and over, each time using a different set of random values from the probability functions.

How do you calculate value at risk?

Value at Risk (VAR) can also be stated as a percentage of the portfolio i.e. a specific percentage of the portfolio is the VAR of the portfolio. For example, if its 5% VAR of 2% over the next 1 day and the portfolio value is $10,000, then it is equivalent to 5% VAR of $200 (2% of $10,000) over the next 1 day.

How do you read a CVaR?

Understanding Conditional Value at Risk (CVaR) While VaR represents a worst-case loss associated with a probability and a time horizon, CVaR is the expected loss if that worst-case threshold is ever crossed. CVaR, in other words, quantifies the expected losses that occur beyond the VaR breakpoint.

What are the advantages and disadvantages of Monte Carlo simulation?

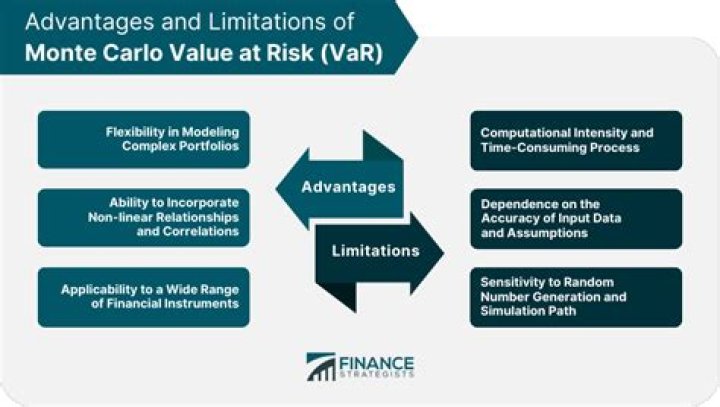

The advantage of Monte Carlo is its ability to factor in a range of values for various inputs; this is also its greatest disadvantage in the sense that assumptions need to be fair because the output is only as good as the inputs.

Why is Monte Carlo risk analysis useful?

Monte Carlo analysis is useful because many investment and business decisions are made on the basis of one outcome. In other words, many analysts derive one possible scenario and then compare that outcome to the various impediments to that outcome to decide whether to proceed.

What is the formula for VaR?

Since the definition of the log return r is the effective daily returns with continuous compounding, we use r to calculate the VaR. That is VaR= Value of amount financial position * VaR (of log return).

Why are Monte Carlo simulations misleading?

Current Monte Carlo software treats uncertainty as if it were variability, which may produce misleading results. Ignoring correlations among exposure variables can bias Monte Carlo calculations. However, information on possible correlations is seldom available.

Why do we use the Monte Carlo simulations?

Monte Carlo simulations are used to model the probability of different outcomes in a process that cannot easily be predicted due to the intervention of random variables. It is a technique used to understand the impact of risk and uncertainty in prediction and forecasting models.

What is Monte Carlo risk analysis?

Monte Carlo Risk Analysis is an approach to performing risk analysis on any project with uncertain input data. Generally, numbers are selected from representative input data and then used in iterative, CPU-intensive calculations to find the most likely outcome and the range of probable outcomes.

What is Monte Carlo simulation analysis?

Monte Carlo simulation performs risk analysis by building models of possible results by substituting a range of values-a probability distribution-for any factor that has inherent uncertainty. It then calculates results over and over, each time using a different set of random values from the probability functions.