ERISA establishes guidelines and minimum standards designed to protect employees of private sector companies who participate in retirement and welfare benefit plans. Businesses administering a qualified retirement plan that aren’t in full compliance with ERISA could be subject to costly penalties.

Who has to comply with ERISA?

ERISA applies to private-sector companies that offer pension plans to employees. This includes businesses that: Are structured as partnerships, proprietorships, LLCs, S-corporations and C-corporations. No matter how your employer has structured his or her business, it is covered by ERISA if it is a private entity.

What plans are exempt from ERISA?

Governmental and church plans are exempt from ERISA’s mandates. Also exempt are programs maintained solely to comply with state-law requirements for workers’ compensation, unemployment compensation, or disability insurance, as are plans maintained outside the United States for nonresident aliens.

What protections does ERISA provide to employees in general?

ERISA prohibits fiduciaries from misusing funds and also sets minimum standards for participation, vesting, benefit accrual, and funding of retirement plans. It also grants retirement plan participants the right to sue for benefits and breaches of fiduciary duty.

What benefits are covered by ERISA?

ER2. What arrangements are covered by ERISA?

- health insurance.

- group life insurance.

- long-term disability income.

- severance pay.

- funded vacation benefits, apprenticeship or other training programs, or day care centers, scholarship funds, or prepaid legal services; and.

How will you comply with ERISA?

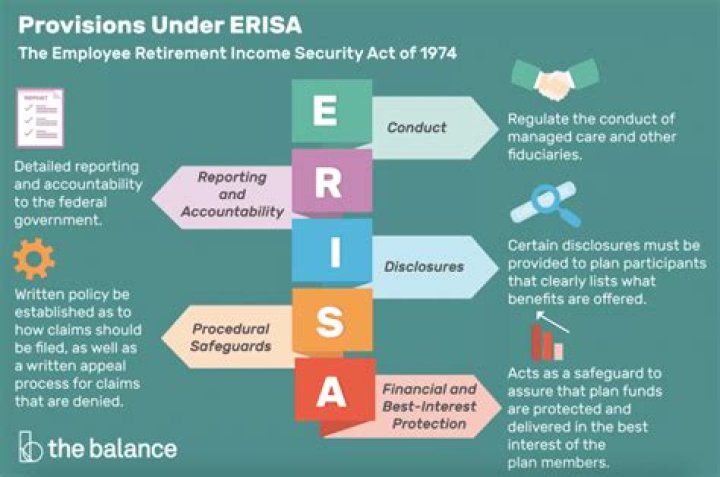

Primary responsibilities for employers to comply with ERISA include three important items: Detailed disclosure to covered individuals (plan participants and beneficiaries). A strict fiduciary code of conduct for plan sponsors. Detailed reporting through Form 5500, as applicable.

What employers are exempt from ERISA?

The ERISA exemptions that do exist include: Insurance policies and benefits issued by government employers or entities. This includes local government, city government, state government and the federal government. If you work for the government in any capacity, your pension and benefits are likely not covered by ERISA.

How do you file an ERISA complaint?

For technical assistance and complaints, you should call EBSA’s toll free number at 1-866-444-3272. You may contact us electronically at Please note: The law is not all-encompassing and you may not always be pleased with the remedy or with the explanation you receive.

How do I report an ERISA violation?

Contact your regional EBSA office to file a complaint or an appeal after exhausting your insurance appeals process. You can also find ERISA information through the U.S. Department of Labor online at

What does ERISA regulate?

The Employee Retirement Income Security Act (ERISA) is a federal law that regulates and establishes oversight for private industry pension plans, retirement plan, profit-sharing plans and health insurance coverage by establishing rules and minimum standards that are meant to protect plan participants.

ERISA only exempts two types of employers: Employee benefit plans maintained by governmental employers are exempt from ERISA’s requirements. This exemption includes plans maintained by the federal, state or local (for example, a city, county or township) governments. Church plans are also exempt from ERISA.

What protections does ERISA provide?

ERISA is the acronym for The Employee Retirement Income Security Act and was enacted by the 93rd United States Congress on September 2, 1974. Designed to provide pension reform, the act is a federal law that sets standards and regulations of protection for individuals that are in private sector company retirement plans.

What is ERISA and does it apply?

ERISA is a federal law. It applies to many private employers and establishes minimum standards for health, retirement (pension plans), and other welfare benefit plans, such as life insurance, disability insurance, or apprenticeship plans. These minimum standards protect not only employees but also employers.