A Bermuda swaption is a variation of a regular (“vanilla”) swaption that gives the holder the right, but not the obligation, to enter into an interest rate swap on any one of many predetermined dates.

How do you value a Bermuda swaption?

Find the underlying interest rate swap value at each final note. Conduct backward induction process iteratively rolling back from final dates until reaching the valuation date. Compare exercise values with intrinsic values at each exercise date. The value at the valuation date is the price of the Bermudan swaption.

How are swaptions priced?

The valuation of swaptions is complicated in that the at-the-money level is the forward swap rate, being the forward rate that would apply between the maturity of the option—time m—and the tenor of the underlying swap such that the swap, at time m, would have an “NPV” of zero; see swap valuation.

What is Swaption with an example?

For example, if current market rates are 6%, you would pay more for a Swaption at 7% than a Swaption at 8.5%. The premium on a Swaption also depends on the rollover frequency and how you make your premium payments.

What is callable swap?

A callable swap is a contract between two counterparties in which the exchange of one stream of future interest payments is exchanged for another based on a specified principal amount. These swaps usually involve the transfer of the cash flows from a fixed interest rate for the cash flows of a floating interest rate.

What is a Bermuda call?

Bermuda Call: The issuer of the bond may only call a bond on interest payment dates. Make-Whole Call: The issuer of this type of bond may call the bond before the maturity date at par plus a make whole premium.

What is a cancellable swap?

A cancellable swap is a combination of an interest rate swap and a receiver’s swaption that may be cancelled by the borrower at no cost on an agreed future date.

What is swaption interest?

Interest rate swaps are forward contracts where one stream of future interest payments is exchanged for another based on a specified principal amount. Interest rate swaps can exchange fixed or floating rates in order to reduce or increase exposure to fluctuations in interest rates.

How does an interest rate swaption work?

With an interest rate swap, the borrower still pays the variable rate interest payment on the loan each month. Then, the borrower makes an additional payment to the lender based on the swap rate. The swap rate is determined when the swap is set up with the lender and is unchanging from month to month.

What is a swaption price?

An interest rate swaption is an option that provides the borrower with the right but not the obligation to enter into an interest rate swap on an agreed date(s) in the future on terms protected by the swaption. The buyer/borrower and seller agree the price, expiration date, amount and fixed and floating rates.

What are the terms of a Bermuda swaption?

The terms of the swaption also spell out if the buyer is going to pay the floating rate or the fixed rate. A Bermuda swaption gives the buyer the option to engage in an interest rate swap on a specified date during the life of the option.

What is the difference between vanilla swaptions and writings of Bermuda?

Writers of Bermuda swaptions can have more control over the exercising of the swaptions. Pricing of such swaptions is more complex than vanilla swaptions. With the inclusion of more potential exercise dates, the calculations become more complicated.

What type of cash flows are exchanged in a Bermuda swap?

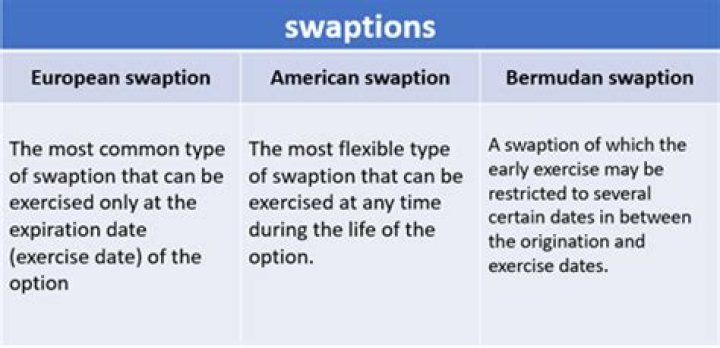

Only cash flows are exchanged in this swap. The exercise feature of Bermuda swaptions falls somewhere between American and European styles. Holders may exercise American-style options and swaptions at any time between the issue and the expiration dates. Holders may utilize European-style options and swaptions only at maturity.

What is a Bermuda option?

A Bermuda option is a type of exotic contract that can only be exercised on predetermined dates. A swaption, also known as a swap option, refers to an option to enter into a swap agreement with another party.