You need at least a 15-20% down payment to buy an investment property. That means the max LTV is 80-85%. For an investment property cash out refinance, the max LTV is 70-75% depending on your lender and whether the loan is fixed-rate or adjustable-rate.

What is a good maximum loan to value ratio?

For a home mortgage, the maximum loan-to-value ratio is typically 80%. Higher loan-to-value ratios may require a borrower to purchase insurance to protect the lender or result in higher interest rates.

How do you calculate LTV on real estate?

To figure out your LTV ratio, divide your current loan balance (you can find this number on your monthly statement or online account) by your home’s appraised value. Multiply by 100 to convert this number to a percentage.

What is the lowest loan to value mortgage?

The lowest LTV mortgages available come with a ratio of 60%, going right up to 100% for the highest. Below 80% is considered ‘low’, with 85-90% and upwards considered ‘high’. Low LTV mortgages come with low interest rates but high deposits, and vice versa for loans with high ratios.

What is DTI in real estate?

Your debt-to-income ratio (DTI) compares how much you owe each month to how much you earn. Specifically, it’s the percentage of your gross monthly income (before taxes) that goes towards payments for rent, mortgage, credit cards, or other debt.

What is PITI in real estate?

PITI is an acronym that stands for principal, interest, taxes and insurance. Many mortgage lenders estimate PITI for you before they decide whether you qualify for a mortgage.

How do I calculate the loan to value ratio?

Calculating your loan-to-value ratio

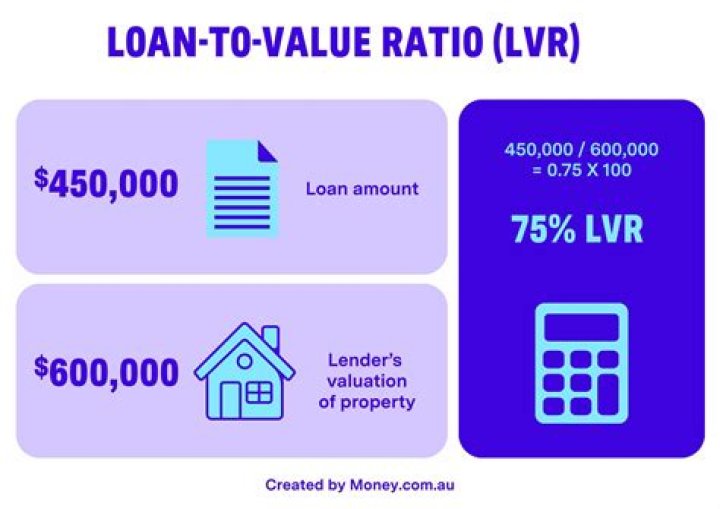

- Current loan balance ÷ Current appraised value = LTV.

- Example: You currently have a loan balance of $140,000 (you can find your loan balance on your monthly loan statement or online account).

- $140,000 ÷ $200,000 = .70.

- Current combined loan balance ÷ Current appraised value = CLTV.

What is the lowest loan-to-value mortgage?

Is 55% a good LTV?

A 55% LTV mortgage is at the low end of the typical range – usually, lenders offer LTVs between 50% and 95%. With a 55% LTV, lenders are taking on less of a risk, so you’ll have a wide range of competitive options to choose from, with better deals and a lower total cost than you would with higher LTVs.

What is the loan-to-value ratio of a property?

The loan-to-value (LTV) ratio of a property is the percentage of the property’s value that’s mortgaged. Lenders use different requirements to determine whether a loan will be granted, and the LTV is usually a key factor.

What is a good LTV ratio for a mortgage loan?

In general, lenders are willing to lend at CLTV ratios of 80% and above to borrowers with high credit ratings. The LTV ratio considers only the primary mortgage balance. Therefore, in the above example, the LTV ratio is 50%, the result of dividing the primary mortgage balance of $100,000 by the home value of $200,000.

Should you lower your loan-to-value ratio?

You probably care less about your lender’s finances than your own purse strings, and that makes sense. You might not want to part with a lot of cash at closing by putting more money down to lower your LTV ratio, but a lower LTV has several advantages over the long term.

How low can your loan-to-value ratio go before MIP expires?

FHA loans, which allow an initial LTV ratio of up to 96.5%, require a mortgage insurance premium (MIP) that lasts for as long as you have that loan no matter how low the LTV ratio eventually goes. Most people refinance to a conventional loan once the LTV ratio reaches 80% to eliminate the MIP.