Section 197(d)(1) provides that the term “section 197 intangible” means (A) goodwill; (B) going concern value; (C) any of the following intangible items: (i) workforce in place including its composition and terms and conditions (contractual or otherwise) of its employment, (ii) business books and records, operating …

What are amortizable intangible assets?

Amortization of intangible assets is a process by which the cost of such an asset is incrementally expensed or written off over time. Intangible assets may include various types of intellectual property—patents, goodwill, trademarks, etc.

What is the recovery period for section 197 intangibles?

You must generally amortize over 15 years the capitalized costs of “section 197 intangibles” you acquired after August 10, 1993. You must amortize these costs if you hold the section 197 intangibles in connection with your trade or business or in an activity engaged in for the production of income.

What is charged on intangible assets?

Intangible Assets acquired Free of Charge or for a Nominal Consideration by way of Government Grant. In that case an entity should, record both the grant and the intangible asset at fair value. As per AS 26, intangible assets is recognised at nominal value or at acquisition cost. 8.

What are Section 197 assets?

Section 197 intangibles are certain intangible assets acquired after August 10, 1993 (or after July 25, 1991, if chosen) in connection with the acquisition of a business which must be amortized over 15 years from the date of acquisition regardless of the assets useful life.

What is a section 197?

Section 197 of the Labour Relations Act (LRA) places heavy responsibilities on the employer who takes over the business (or part thereof) of another employer as a going concern. This section forces the new employer to take over all the labour related obligations of the old employer.

How do you identify intangible assets?

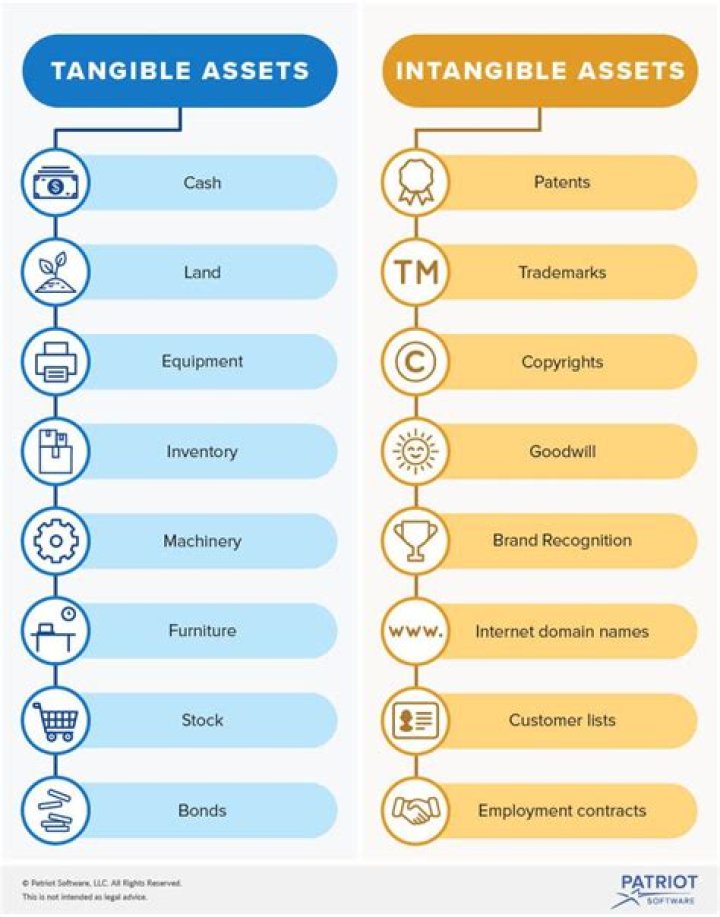

An intangible asset is an asset that is not physical in nature. Goodwill, brand recognition and intellectual property, such as patents, trademarks, and copyrights, are all intangible assets. Intangible assets exist in opposition to tangible assets, which include land, vehicles, equipment, and inventory.

Is goodwill amortizable for tax purposes?

Any goodwill created in an acquisition structured as an asset sale/338 is tax deductible and amortizable over 15 years along with other intangible assets that fall under IRC section 197. Any goodwill created in an acquisition structured as a stock sale is non tax deductible and non amortizable.

When did goodwill become amortizable?

In 2001, a legal decision prohibited the amortization of goodwill as an intangible asset. However, in 2014, parts of this ruling were rolled back; amortization is now allowable in certain situations.

What is an amortizable section 197 intangible?

The term “amortizable section 197 intangible ” does not include any section 197 intangible acquired in a transaction, one of the principal purposes of which is to avoid the requirement of subsection (c) (1) that the intangible be acquired after the date of the enactment of this section or to avoid the provisions of subparagraph (A).

What is section 197-2 amortization of goodwill?

§ 1.197-2 Amortization of goodwill and certain other intangibles. (1) In general. Section 197 allows an amortization deduction for the capitalized costs of an amortizable section 197 intangible and prohibits any other depreciation or amortization with respect to that property.

What is section 197 of the Internal Revenue Code?

Internal Revenue Code § 197. Amortization of goodwill and certain other intangibles (a) General rule. –A taxpayer shall be entitled to an amortization deduction with respect to any amortizable section 197 intangible.

How is the amortization deduction determined under Section 197?

The amortization deduction under section 197 is determined by amortizing basis ratably over a 15-year period under the rules of paragraph (f) of this section. Section 197 also includes various special rules pertaining to the disposition of amortizable section 197 intangibles, nonrecognition transactions, anti-churning rules, and anti-abuse rules.