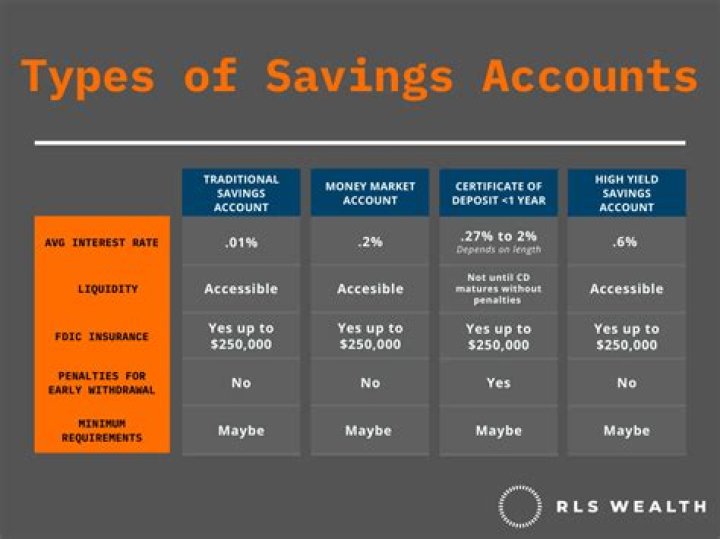

The 3 common savings account types are regular deposit, money market, and CDs. Each one works a little different regarding accessibility and amount of interest. Besides these accounts, there are other savings options too.

Is it OK to have 3 savings accounts?

There is no magic number. The amount of savings accounts that is right for you depends on your personal finances. If you have lots of money, you will want to open multiple bank accounts to make sure all of your cash is insured, for example. There is no limit to how many savings accounts you can have.

What are some examples of savings plans?

When it comes to saving money, you can choose between several different savings plans.

- Savings account.

- Individual Retirement Account (IRA)

- Investment trading account.

- Certificate of Deposit (CD)

- 529 savings plan.

What are the best savings plans?

Best Saving Plans

- National Savings Certificate.

- Senior Citizen Savings Scheme.

- Recurring Deposits.

- Post Office Monthly Income Scheme (MIS)

- Public Provident Fund (PPF)

- KVP (Kisan Vikas Patra)

- Sukanya Samriddhi Yojana (SSY)

- Atal Pension Yojana.

What are 4 types of savings accounts?

Basic Savings Account. Also known as passbook savings accounts, these accounts are a good introduction to earning interest and saving money.

How many savings should I have?

Experts advise individuals to save at least three months worth of living expenses – the majority of people in the UK are not at this recommended level. There can be multiple reasons for not saving enough, but insufficient earnings are always among the top reasons.

Is it a good idea to open multiple savings accounts?

“Having more than one savings account is a good idea because it creates a specific plan for your money,” Schulte says. If you’re trying to accomplish multiple savings goals, opening multiple bank accounts may be the right plan for you.

What is a saving plan?

The phrase “savings plan” is just a way to describe the process of saving enough money to buy a home — or saving for any other life goal that’s important to you. It’s a strategic process that allows you to make measurable, sustainable, and consistent progress toward what you want.

How do I choose a savings plan?

There are a few things you’ll want to consider to figure out which savings account you should open:

- Decide how you’ll use it.

- Figure out what’s important to you.

- Decide whether you want to use your existing bank.

- Consider interest rates.

- Read the fine print for fees.

- Don’t put too much pressure on your decision.

What is a savsavings plan?

Savings Plans are a flexible pricing model that offer low prices on EC2, Lambda, and Fargate usage, in exchange for a commitment to a consistent amount of usage (measured in $/hour) for a 1 or 3 year term. When you sign up for a Savings Plan, you will be charged the discounted Savings Plans price for your usage up to your commitment.

Are there any 52 Week savings plans that actually work?

Actually, I came up with 3 new 52 week savings plans that just might work out better in the long run. This is the easiest way to use the 52 week savings plan from last year, and not feel burned out at the end of this year. It seems really easy to save a small amount per week, until summer (and your vacations) start to hit that checking account.

What is a Fifth Third savings account?

A straightforward account to help you maximize your savings. You have a Fifth Third Checking Account (Does not include Fifth Third Express Banking.). All owners of your savings account must also be listed together as owners on your Fifth Third checking account.

How to make a successful savings plan?

7 tips to a successful savings plan. 1 1. Have a goal. The people who are the most successful at something have a strong ‘why’ behind what they are doing. So, why do you want to save 2 2. Know where you stand. 3 3. Create a plan. 4 4. Monitor your spending. 5 5. Refine your spending habits.