How to Calculate MACRS Depreciation

- Determine your basis, namely the original value of that asset.

- Determine your property’s class.

- Determine your depreciation method.

- Choose your MACRS depreciation convention, namely the time you first started using that asset.

- Determine your percentage.

How do you depreciate MACRS?

When calculating depreciation expense for MACRS, always use the original purchase price of the asset as the depreciable base for each period. Note that you depreciate each category for one year longer than its classification period. For example, depreciate an asset classified under 3-Year MACRS for 4 years.

What is MACRS property?

MACRS stands for the Modified Accelerated Cost Recovery System. Thus, MACRS is the depreciation system used for real and personal property associated with commercial or residential real estate, and MACRS assigns a specific asset class that dictates the depreciable life of that asset.

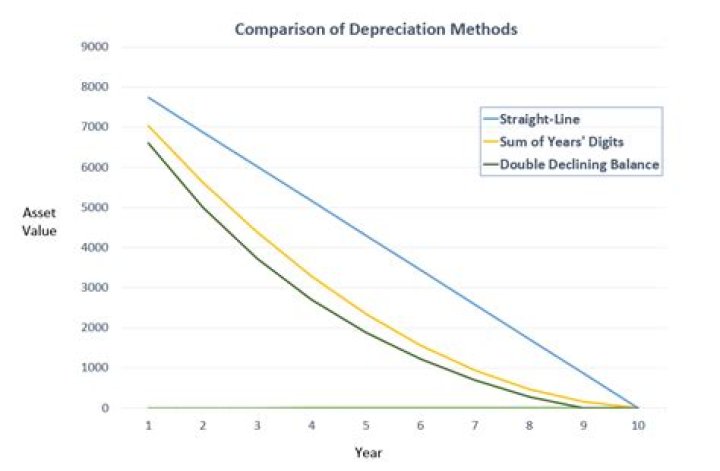

What are the five methods of depreciation?

There are five methods of Depreciation, such as:

- Straight-line method.

- Unit of Production Method.

- Reducing balancing method.

- Double declining balance method.

- Sum-of the year’s Digits method.

How do you do MACRS depreciation?

In MACRS straight line, LN calculates the percentage for a year by dividing one depreciation period by the remaining life of the asset, and then applying this amount with the averaging convention to determine the depreciation amount for that year.

What is convention in depreciation?

Depreciation conventions are used to determine when and how depreciation is calculated for both the year when the fixed asset is acquired and the year when the fixed asset is disposed of. Depreciation conventions can also be set on an individual fixed asset book.

What is MACRS 5 year depreciation?

MACRS is an accelerated depreciation system. An asset is to be depreciated with MACRS using a 5-year recovery period. The first year of recovery is based on double-declining-balance depreciation for one-half year. Verify by an appropriate calculation that r1 for this recovery period is 20.00%.

Why are there different methods of depreciation?

Depending on the type of company, different methods of depreciation may come to bear to determine the current value of company assets. It may be more advantageous to depreciate equipment earlier in its use, equally over time, or closer to the end of its expected use.

What is the difference between MACRS, ACRs and non-recovery?

What is the difference between macrs, acrs and non-recovery. MACRS applies to most depreciable property placed in service in 1987 or later. ACRS is for property placed in service in 1981-1987. Nonrecovery property examples are movies, pre 1987 property. 0.

What are the different methods of depreciation in accounting?

First, among types of depreciation methods is the straight-line method, also known as the Original cost method, Fixed instalment method, and Fixed percentage method. Simplest, most used and popular method of charging depreciation is the straight-line method. An equal amount is allocated in each accounting period.

What is the formula for depreciation expense?

Depreciation expense is calculated using this formula: (cost basis minus residual value) divided by the number of years of the asset’s expected useful life.

What is accelerated cost recovery system?

Accelerated Cost Recovery System (ACRS) The Accelerated Cost Recovery System (ACRS) is a method of depreciating property for tax purposes; it allows individuals and businesses to write off capitalized assets in an accelerated manner.