To calculate FIFO (First-In, First Out) determine the cost of your oldest inventory and multiply that cost by the amount of inventory sold, whereas to calculate LIFO (Last-in, First-Out) determine the cost of your most recent inventory and multiply it by the amount of inventory sold.

What is LIFO FIFO with example?

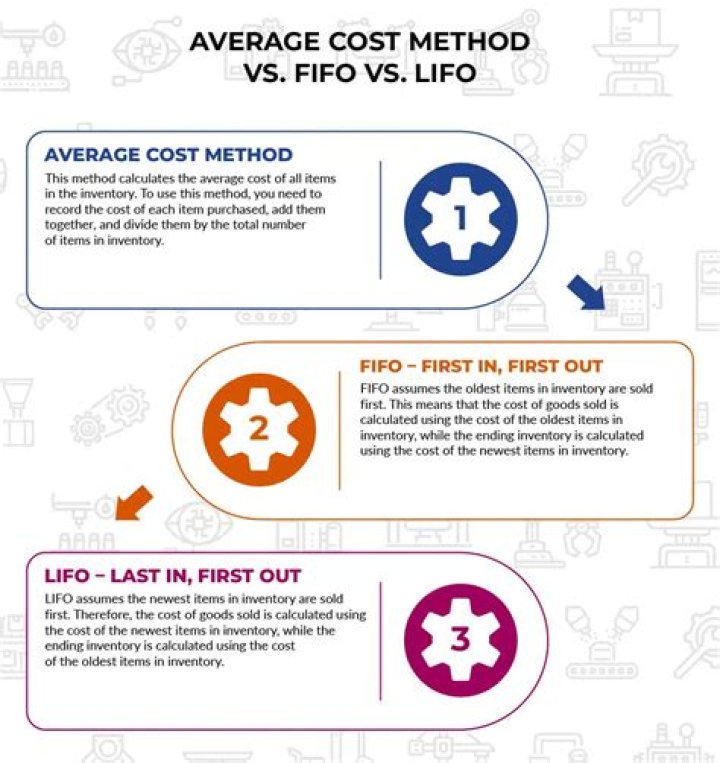

FIFO (“First-In, First-Out”) assumes that the oldest products in a company’s inventory have been sold first and goes by those production costs. The LIFO (“Last-In, First-Out”) method assumes that the most recent products in a company’s inventory have been sold first and uses those costs instead.

Which is better FIFO LIFO or average cost?

Generally speaking, FIFO is preferable in times of rising prices, so that the costs recorded are low, and income is higher. Contrarily, LIFO is preferable in economic climates when tax rates are high because the costs assigned will be higher and income will be lower.

How do you calculate FIFO average cost?

It is calculated by dividing the total number of units you have on hand by the total cost of goods. You will arrive at an average unit cost for each unit of your inventory.

What is LIFO in cost accounting?

Last in, first out (LIFO) is a method used to account for inventory. Under LIFO, the costs of the most recent products purchased (or produced) are the first to be expensed. LIFO is used only in the United States and governed by the generally accepted accounting principles (GAAP).

What is the difference between FIFO and average cost?

Average Costing is used to track inventory costing via ‘average’ cost, or by averaging the costs of all the quantities that are in stock divided by the total cost of those purchases. The FIFO Method assumes that inventory purchased or manufactured first is sold first and that the newest inventory remains unsold.

What is average cost method inventory?

The average cost method assigns a cost to inventory items based on the total cost of goods purchased or produced in a period divided by the total number of items purchased or produced. The average cost method is also known as the weighted-average method.

When to use LIFO?

The LIFO method is sometimes used by computers when extracting data from an array or data buffer. When a program needs to access the most recent information entered, it will use the LIFO method. When information needs to be retrieved in the order it was entered, the FIFO method is used. Updated: February 23, 2007.

Who uses LIFO inventory method?

The last in, first out (LIFO) method is used to place an accounting value on inventory. The LIFO method operates under the assumption that the last item of inventory purchased is the first one sold.

What is FIFO in inventory?

FIFO is an accounting method for counting inventory. This is also used as a method for business management, as well. FIFO means treating the inventory as the first products in are the first products sold.

What is the LIFO method?

LIFO, which stands for last-in-first-out, is an inventory valuation method which assumes that the last items placed in inventory are the first sold during an accounting year. The default inventory cost method is called FIFO (First In, First Out), but your business can elect LIFO costing. LIFO accounting is only used in the United States.