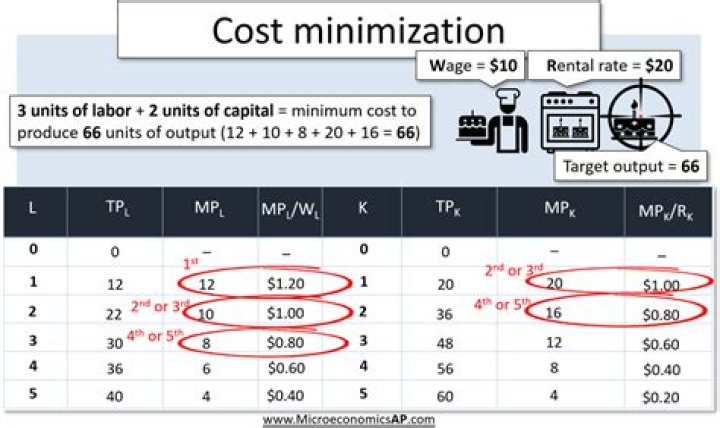

The Cost-Minimization Rule Cost is minimized at the levels of capital and labor such that the marginal product of labor divided by the wage (w) is equal to the marginal product of capital divided by the rental price of capital (r).

How do you know if MPL is diminishing?

In its most simplified form, diminishing marginal productivity is typically identified when a single input variable presents a decrease in input cost. A decrease in the labor costs involved with manufacturing a car, for example, would lead to marginal improvements in profitability per car.

What level of q minimizes total cost?

The level of Q that minimizes total cost is MC(Q) = 4Q = 0, or Q = 0. g. Net benefits are maximized when MNB(Q) = MB(Q) – MC(Q) = 0, or 20 – 4Q – 4Q = 0. Some algebra leads to Q = 20/8 = 2.5 as the level of output that maximizes net benefits.

What output level minimizes average total cost?

c) To determine the quantity to be produced in order to minimize the average total costs we have to calculate the quantity that makes marginal costs equal average total costs. So, ATC is minimized at 50 units of output.

What is cost minimization in economics?

Cost minimization simply implies that firms are maximizing their productivity or using the lowest cost amount of inputs to produce a specific output. In the short run firms have fixed inputs, like capital, giving them less flexibility than in the long run. This lack of flexibility in the choice of inputs tends to result in higher costs.

How do you choose k and L to minimize total costs?

A firm is assumed to choose k and l to minimize total costs. The condition for this minimization is that the rate at which k and l can be traded technically (while keeping q ¼ q. 0) should be equal to the rate at which these inputs can be traded in the market.

What are some real life examples of cost minimizing decisions?

In that case the cost minimizing decision is actually to use the higher yielding corn variety and rent out the unused land. Another classic example is that of a small business owner who runs, say, a coffee shop. The inputs into the coffee shop are the labor, the coffee, the electricity, the machines and so on.

How do firms maximize profits in the short run?

In order to maximize profits firms must minimize cost. Cost minimization simply implies that firms are maximizing their productivity or using the lowest cost amount of inputs to produce a specific output. In the short run firms have fixed inputs, like capital, giving them less flexibility than in the long run.