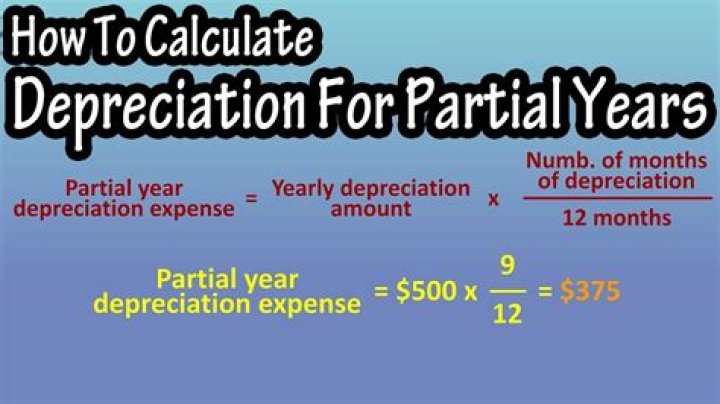

The simple rules for calculating depreciation of an asset placed in service during a short tax year are:

- Determine the depreciation for a full tax year.

- Multiply he depreciation in step 1 by a fraction. The numerator (top number) of the fraction is the number of months the property is in service.

How do you calculate depreciation for 12 months?

First subtract the asset’s salvage value from its cost, in order to determine the amount that can be depreciated.

- Total depreciation = Cost – Salvage value.

- Annual depreciation = Total depreciation / Useful lifespan.

- Monthly depreciation = Annual deprecation / 12.

- Monthly depreciation = ($1,200/5) / 12 = $20.

Does short year depreciation affect half year convention?

In a short tax year, depreciation is allowable only for that part of the tax year the property is treated as in service. For the half-year convention, a taxpayer is required to treat property as placed in service or disposed of on either the first day or the midpoint of a month.

How do you calculate MACRS depreciation on rental property?

31, 2017, or 40 years if placed in service prior to that. Next, determine the amount that you can depreciate each year. As most residential rental property uses GDS, we’ll focus on that calculation….Which System to Use.

| January | 3.485% |

|---|---|

| February | 3.182% |

| March | 2.879% |

| April | 2.576% |

| May | 2.273% |

Is bonus depreciation an election?

Election Out of Bonus Depreciation In general, taxpayers may elect out of bonus depreciation for any qualifying property placed in service during the taxable year. The election applies to all property of the same property class that is placed in service by the taxpayer in the same year.

How do I calculate bonus depreciation?

Bonus depreciation is calculated by multiplying the bonus depreciation rate (currently 100%) by the cost basis of the acquired asset. For a business that claims bonus depreciation on an item that costs $100,000, for example, the resulting deduction would be worth $21,000, assuming the company’s tax rate is 21%.

How do you calculate depreciation per year?

Simply divide the asset’s basis by its useful life to find the annual depreciation. For example, an asset with a $10,000 basis and a useful life of five years would depreciate at a rate of $2,000 per year.

How is depreciation calculated in the MACRS depreciation calculator?

The MACRS Depreciation Calculator uses the following basic formula: D i = C × R i. Where, D i is the depreciation in year i; C is the original purchase price, or basis of an asset; R i is the depreciation rate for year i, depends on the asset’s cost recovery period

What does MACRS stand for?

The Modified Accelerated Cost Recovery System, or MACRS is the primary method of depreciation for federal income tax purposes allowed in the U.S. to determine depreciation deductions. The MACRS system of depreciation allows for larger depreciation deductions in the early years and lower deductions in…

What is modified accelerated cost recovery system depreciation?

The IRS introduced the Modified Accelerated Cost Recovery System (MACRS), a depreciation method used for accounting purposes, in 1986. Very simply, the general MACRS depreciation formula allows for a larger tax deduction in the early years of an asset’s useful life and less as time goes by.

What is the mid-quarter convention for depreciation?

The mid-quarter convention should only be used if more than 40% of your depreciable assets are purchased during the last 3 months of the tax year. You get half-a-year’s worth of depreciation no matter how long you used that asset during the year.