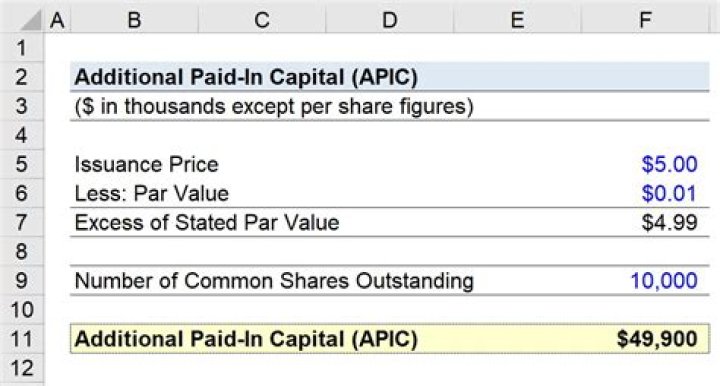

Additional paid-in capital is recorded in the shareholders’ equity portion of a company’s balance sheet. The APIC formula is APIC = (Issue Price – Par Value) x Number of Shares Acquired by Investors.

Is treasury stock recorded as additional paid-in capital?

Thus, the Treasury Stock account is debited at cost when shares are acquired and credited at cost when these shares are sold. Any excess of the reissue price over cost represents additional paid-in capital and is credited to Paid-In Capital—Common (Preferred) Treasury Stock.

Does treasury stock include par value?

What Is the Cost Method of Accounting for Treasury Stock? The cost method uses the value paid by the company during the repurchase of the shares and ignores their par value. Under this method, the cost of the treasury stock is included within the stockholders’ equity portion of the balance sheet.

What is par value of treasury stock?

The par value method is based on the assumption that the acquisition of treasury stock is essentially a permanent reduction in stockholders’ equity. The entries used in the method are thus structured as if the shares have been retired.

What is Additional paid up capital?

Definition: Additional paid-in capital (APIC) is the amount of money that a company’s shareholders pay for shares in excess of the par value of the shares. In other words, it’s the amount over the par value that investors are willing to pay for the stock.

Is common stock part of paid in capital?

Common stock is a component of paid-in capital, which is the total amount received from investors for stock. On the balance sheet, the par value of outstanding shares is recorded to common stock, and the excess (market price-par value) is recorded to additional paid-in capital.

What is additional paid in capital?

Additional paid-in capital (APIC) is the difference between the par value of a stock and the price that investors actually pay for it. To be the “additional” part of paid-in capital, an investor must buy the stock directly from the company during its IPO.

Which type of capital is issued at par value?

The total value of the shares a company elects to sell to investors is called its issued share capital. The par value of the issued share capital cannot exceed the value of the authorized share capital.

How do you increase additional paid in capital?

How to Increase Additional Paid-In Capital. The recorded amount of additional paid-in capital can only increase when an issuer sells more stock to investors, where the price at which the shares are sold exceeds the par value of the shares.

How does Additional paid in capital decrease?

What is Additional Paid In Capital? Additional Paid In Capital (APIC) is the value of share capital above its stated par value and is an accounting item under Shareholders’ Equity on the balance sheet. APIC can be created whenever a company issues new shares and can be reduced when a company repurchases its shares.

What is the difference between par value and additional paid in capital?

The par value for a share is printed on the stock certificate. Additional paid-in-capital is the amount investors have paid the company over and above par value. It is important to note that additional paid-in-capital is only recorded at the initial public offering.

What is the par value method for the purchase of treasury stock?

Purchase of treasury stock – par value method. When a company purchases its own shares and uses par value method for accounting purpose, the treasury stock account is debited with the total par value of shares acquired and cash account is credited with the amount of cash paid. If the debit part of the journal entry exceeds the credit part,…

What is additional paid-in capital (APC)?

December 14, 2018/. Additional paid-in capital is any payment received from investors for stock that exceeds the par value of the stock. The concept applies to payments received for either common stock or preferred stock.

What is the price of par Vale common stock per share?

Issued 2,000 shares of $5 par vale common stock at $20 per share. Bought back 300 shares at $18 per share. Bought back 400 shares at $25 per share. Reissued 200 shares at $30 per share.