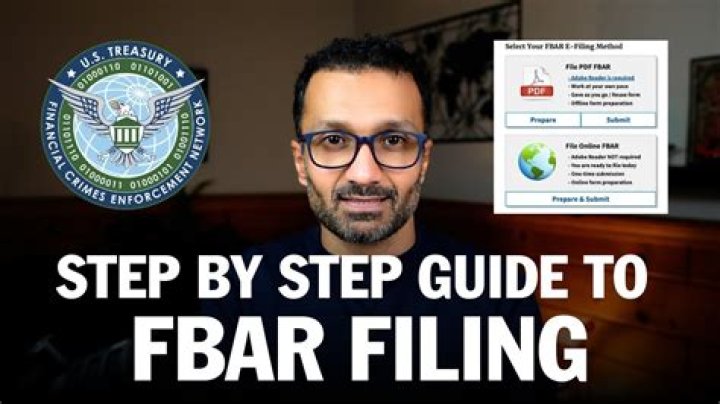

You must file the FBAR electronically through the Financial Crimes Enforcement Network’s BSA E-Filing System. You don’t file the FBAR with your federal tax return. If you want to paper-file your FBAR, you must call FinCEN’s Regulatory Helpline to request an exemption from e-filing.

Can I file FBAR yourself?

Bank & Financial Accounts (FBAR) To file the FBAR as an individual, you must personally and/or jointly own a reportable foreign financial account that requires the filing of an FBAR (FinCEN Report 114) for the reportable year. There is no need to register to file the FBAR as an individual.

What is the deadline for FBAR 2021?

October 15, 2021

IRS reminds FBAR filers about October 15, 2021 extension deadline. In a news release (IR-2021-96), the IRS is reminding US citizens, resident aliens and domestic legal entities that the extension deadline to file an annual Report of Foreign Bank and Financial Accounts (FBAR) is October 15, 2021.

Is it easy to file FBAR?

The FBAR is filed separately to the Department of the Treasury–not the IRS. To file the FBAR, you’ll use FinCEN 114 and submit it electronically through the BSA e-filing site. The process is straightforward and requires you to gather all pertinent account information and enter it into the online system.

Do I need to file FBAR every year?

If you want to avoid tax penalties , make sure to file FinCEN Form 114 timely. The FBAR deadline is April 15 following the calendar year you’re reporting. If you’re required to file, you must file one every year.

Is Filing FBAR easy?

Should I file FBAR every year?

What happens if you forget to file FBAR?

If the IRS determines that you committed a willful violation, it means that you did know about the requirement to file an FBAR and still chose not to report your foreign bank accounts. The consequence of this determination can include a penalty of $100,000 or 50% of the account value, whichever is higher.

Do I pay tax on FBAR?

Keep in mind that those filing FBAR aren’t taxed on the balance of the accounts or anything of the sort–it’s truly just a reporting requirement so that the IRS knows what money lies overseas.

What happens if you dont file FBAR?

Failing to file an FBAR can carry a civil penalty of $10,000 for each non-willful violation. But if your violation is found to be willful, the penalty is the greater of $100,000 or 50 percent of the amount in the account for each violation—and each year you didn’t file is a separate violation.

What is FBAR and who must file a FBAR?

What is FBAR? What is FBAR? FBAR stands for Foreign Bank Account Report, which is also known as FinCEN form 114. Who must file an FBAR? According to the IRS, those who must file an FBAR are: A U.S citizen or resident; An entity (corporation, limited liability company, partnership) legally When are you exempt from filing an FBAR?

Should you file FBAR for the first time?

But one should consider where you are going long term with your issues, how quickly you plan to act, and whether you have good and accurate information to file now. If you are just addressing foreign accounts and income for the first time, filing a first FBAR on time may even be a mistake.

Who is required to file a FBAR?

Who Must File an FBAR. United States persons are required to file an FBAR if: the United States person had a financial interest in or signature authority over at least one financial account located outside of the United States; and.

Who must file a FBAR?

Who Must File an FBAR. United States persons are required to file an FBAR if: The United States Person had a financial interest in or signature authority over at least one financial account located outside of the United States and.